This week, the total inventory of construction steel continued to decline. The total inventory of rebar decreased by 5.94% WoW, while the total inventory of wire rod decreased by 7.27% WoW. On the supply side, stimulated by rumors of crude steel production cuts, spot prices in the market initially rose before falling. Profits of blast furnace steel mills expanded, and the resumption of production at some blast furnaces drove a slight increase in construction steel production. According to SMM's weekly maintenance survey, the impact from maintenance on construction steel production this week was 1.1543 million mt, a decrease of 50,000 mt WoW. In terms of EAF steel mills, the operating rate of 50 major electric furnace steel mills producing construction steel nationwide was 38.34%, a decrease of 0.64% from the previous period. The daily average production of construction steel decreased slightly WoW, with overall supply remaining relatively stable. On the demand side, stimulated by rumors of production restrictions, market trading activity improved significantly. Coupled with the restocking drive before the Labour Day holiday, market transactions performed moderately well this week. Overall, with stable supply and increasing demand, the inventory of construction steel continued to decline, showing a relatively healthy performance.

This week, the total inventory of rebar was 6.1678 million mt, a decrease of 389,600 mt WoW, or a 5.94% decline (previous value: -4.24%). Compared to the same period of the previous lunar year, it decreased by 2.0731 million mt, or a 25.16% decline (previous value: -23.18%).

Chart-1: Overview of Rebar Inventory

Data source: SMM

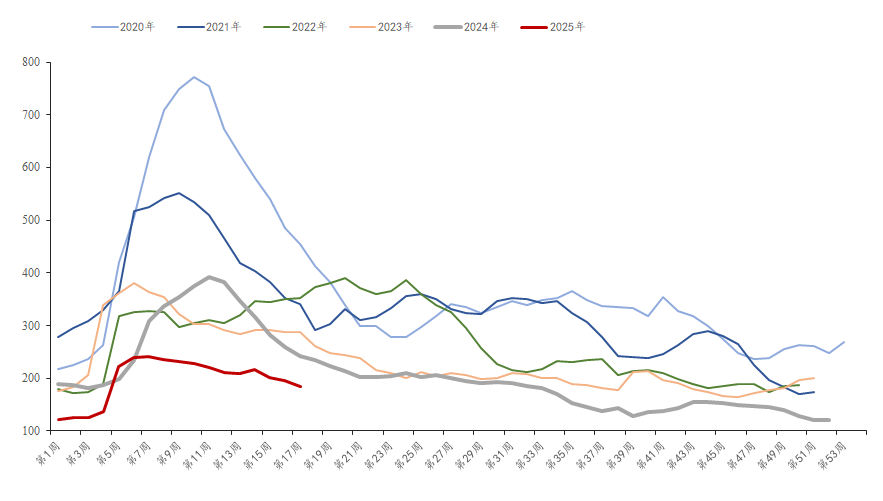

This week, the in-plant inventory of rebar was 1.8341 million mt, a decrease of 112,500 mt from the previous week, or a 5.78% WoW decline (previous value: -3.40%). It decreased by 391,300 mt YoY, or a 17.58% YoY decline (previous value: -16.67%). As the Labour Day holiday approached this week, agents engaged in restocking before the holiday, leading to active inventory reduction at steel mills. However, considering that agents have largely completed their pre-holiday restocking, and that production resumptions at steel mills will outnumber maintenance during the Labour Day holiday, resulting in a slight increase in construction steel supply, it is expected that the pace of inventory reduction at steel mills may slow down after the holiday.

Chart-1: Overview of Rebar Inventory Trends at Steel Mills from 2020 to 2025

Data source: SMM

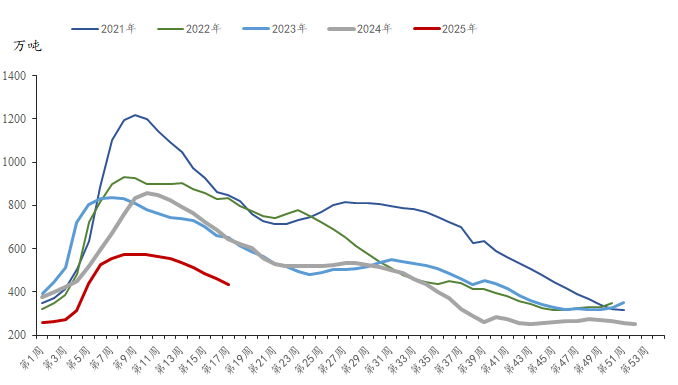

This week, the social inventory of rebar was 4.3337 million mt, a decrease of 277,100 mt from the previous week, or a 6.01% WoW decline (previous value: -4.59%). It decreased by 1.6818 million mt YoY, or a 27.96% YoY decline (previous value: -25.63%). Rumors of production restrictions resurfaced in the market this week, significantly boosting market sentiment and improving speculative demand compared to the previous period. Meanwhile, downstream construction sites engaged in stockpiling before the holiday, with rigid demand shipments performing moderately well. Under these combined influences, social inventory accelerated its decline. However, considering that construction steel transportation and construction site operations may be affected during the Labour Day holiday, with potential reductions in end-use demand, it is expected that the decline in social inventory will narrow after the holiday.

Chart-2: Overview of Rebar Social Inventory Trends from 2021 to 2025

Data source: SMM

Looking ahead, on the supply side, currently, blast furnace steel mills have good export demand for billets, with some manufacturers having nearly full orders for billets from May to June, expecting a reduction in finished steel output. EAF steel mills, constrained by difficulties in acquiring steel scrap and poor profitability, have limited room for production increases. Supply pressure for construction steel in May will ease somewhat. On the demand side, there is still an expected wave of procurement volume releases for projects after the holiday, with demand still worth anticipating. However, considering that some southern cities will gradually enter the rainy season, the overall demand performance in May may not match that of April. Overall, in May, the supply-demand imbalance for construction steel is relatively small, with inventory still having room to decline, but at a slower pace.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)